El Ministerio de Trabajo, Empleo y Seguridad Social (MTESS) aprobó la Resolución Nº 1146/2025, mediante la cual se autoriza la implementación y uso del Sistema Unificado de Asesoramientos y Denuncias (SUAD).

Esta herramienta tecnológica busca centralizar y digitalizar los procesos de atención, registro y seguimiento de asesoramientos y denuncias laborales, fortaleciendo la trazabilidad y la uniformidad de los procedimientos administrativos en todo el territorio nacional.

¿Qué es el SUAD?

El SUAD es la nueva plataforma institucional del MTESS destinada a gestionar de forma integrada los distintos trámites vinculados a la tutela administrativa de los derechos laborales. A través de este sistema, el Ministerio podrá registrar asesoramientos legales, recibir denuncias por incumplimientos laborales, gestionar conciliaciones y derivar casos a fiscalización, aplicando criterios estandarizados de clasificación y priorización.

Entre sus objetivos se destacan:

Unificar en un solo sistema la gestión de asesoramientos, denuncias y actuaciones.

Garantizar la trazabilidad de todos los procesos, desde la recepción hasta la resolución.

Mejorar la calidad de los registros administrativos y la coordinación entre dependencias.

Incorporar herramientas digitales que faciliten la gestión de datos, el control y la transparencia.

Implementación y alcance

El uso del SUAD será obligatorio en todas las dependencias del Ministerio que tramiten asesoramientos y denuncias laborales, quedando prohibida la utilización de registros paralelos fuera de la plataforma.

Su implementación será progresiva, iniciando en la sede central del MTESS y en las direcciones regionales designadas en una primera etapa, hasta extenderse a todo el país.

El sistema operará con dos perfiles principales:

Perfil Administrador, con acceso integral a los módulos del sistema, facultado para validar registros, autorizar actuaciones y derivar los casos a fiscalización o conciliación.

Perfil Operativo, habilitado para registrar asesoramientos, denuncias y conciliaciones, completando los datos requeridos y adjuntando los documentos de respaldo.

Ambos perfiles estarán sujetos a trazabilidad y a deberes de confidencialidad y custodia de la información.

Estructura del sistema

El SUAD está organizado en cuatro módulos principales, que cubren todas las etapas de la gestión administrativa:

Asesoramientos laborales, orientados a brindar orientación técnica y jurídica preventiva a trabajadores o empleadores.

Denuncias laborales, que permiten formalizar la comunicación de incumplimientos normativos e iniciar el procedimiento administrativo.

Conciliaciones laborales, desarrolladas ante la Autoridad Administrativa del Trabajo como mecanismo para resolver conflictos de forma directa y voluntaria.

Actuaciones y derivaciones, módulo interno mediante el cual las denuncias se clasifican y se derivan conforme a su gravedad, reincidencia y tratamiento adecuado (subsanación, conciliación o fiscalización).

Anexos técnicos

La resolución aprueba dos manuales complementarios de aplicación obligatoria para el uso del SUAD:

Anexo I – Manual de Usabilidad del SUAD.

Establece las reglas técnicas y operativas del sistema, describiendo detalladamente la funcionalidad de los cuatro módulos, los procedimientos de registro, los tipos de actuación y los pasos de gestión digital de asesoramientos, denuncias y conciliaciones. Su objetivo es estandarizar criterios, mejorar la calidad de los registros y garantizar la trazabilidad documental en todas las dependencias del Ministerio.

Anexo II – Manual Jurídico de Motivos y Ponderación.

Desarrolla la definición jurídica de 67 motivos de incumplimientos laborales, que abarcan materias como seguridad social, pago de salarios, vacaciones, maternidad, jornada laboral, entre otros.

Cada motivo cuenta con su descripción jurídica, fundamento normativo y nivel de gravedad, dentro de una matriz que va de G1 (crítico) a G6 (leve).

El sistema asigna automáticamente una ponderación a las denuncias en función de la gravedad del hecho y la reincidencia de la empresa, orientando la respuesta institucional más adecuada:

Fiscalización inmediata (G1 y G2).

Conciliación o fiscalización prioritaria (G3 y G4).

Notificación o subsanación (G5 y G6).

Esta herramienta busca asegurar decisiones homogéneas, evitar disparidades en el tratamiento de casos similares y optimizar los recursos institucionales.

Principios de operación y seguridad

El SUAD se rige por los principios de confidencialidad, disponibilidad y seguridad de la información.

La resolución prohíbe expresamente el uso, acceso o divulgación no autorizada de datos, así como la descarga o reproducción de información fuera de los fines previstos.

La Dirección de Tecnología de la Información (DTIC) es responsable de garantizar los controles de acceso, el respaldo periódico de la información y la gestión de vulnerabilidades, mientras que el Observatorio Laboral estará a cargo de la reportería institucional y de los informes estadísticos.

Asimismo, la norma dispone la creación de un esquema de auditoría y mejora continua, con revisiones periódicas sobre calidad de datos y tiempos de gestión, además de un plan de formación obligatoria para los funcionarios que operen el sistema.

Entrada en vigor

El Sistema Unificado de Asesoramientos y Denuncias entrará en vigor el 15 de octubre de 2025, conforme a la Resolución MTESS Nº 1146/2025.

Regulates Law No. 4535/2025 for Micro, Small, and Medium-Sized Enterprises (“ “MIPYMES” for its initials in Spanish”)

Decree No. 4638/2025

September 18, 2025

Paraguay incorporates a new regime of origin within the framework of the Sixty-Ninth (69th) Additional Protocol to Economic Complementation Agreement (“ACE”) No. 35 between the Southern Common Market (“MERCOSUR”) and Chile.

General Resolution No. 36/2025

September 11, 2025

The National Tax Revenue Directorate (“DNIT”) established administrative measures for guarantee trusts.

September – 2025:

► Decree No. 4535/2025 – Law No. 4457/20l2 on MIPYMES is regulated.

The Executive Branch issued Decree No. 4535/2025, which regulates the recently amended and expanded law on the promotion of MIPYMES. The new regulations reinforce the state's commitment to the formalization, competitiveness, and sustainability of a sector that represents the majority of the country's business fabric.

The decree consolidates the role of the Ministry of Industry and Commerce (“MIC”), through its Vice Ministry of MIPYMES, as the authority responsible for coordinating public policies for the development of the sector. Under its direction, a National MIPYMES System is created, which will integrate public, private, and academic entities to implement training, technical assistance, innovation, and access to financing programs.

One of the central points of the regulation is the official classification of MIPYMES, which is established according to their level of turnover and number of workers:

Category

Employees

Annual Turnover

Microenterprises

≤ 10

≤ $ $ 1 billion

Small businesses

11-30

≤ G. 5 billion

Medium-sized companies

31-50

≤ G. 10 billion

This classification is the basis for access to benefits and support programs, as well as for inclusion in the new National Registry of MIPYMES ("RENAMIPYMES"), which will issue the MIPYMES Card, a digital document that certifies formal MIPYMES status and allows access to government incentives.

The decree also regulates the differentiated tax and labor regime introduced in Law No. 7444/25, which provides the following benefits for micro and small enterprises with respect to mandatory taxes related to the exercise of their respective economic activity, corresponding to services provided for registration and authorization by central government agencies and decentralized entities:

Seniority:

≤ 3 years

> 3 years

Microenterprises

Exemption

75% discount

Small businesses

N/A

80% discount

In the labor sphere, more flexible contractual arrangements and a transitional regime are being introduced, allowing micro-enterprises to pay 80% of the minimum wage during their first three years of formal operation.

The regulation also promotes the simplification of procedures through the Unified System for Opening and Closing Businesses (“SUACE”), the digitization of administrative processes, and the creation of financial support mechanisms such as the FONAMIPYMES trust, designed to facilitate access to credit and operating capital.

With these regulations, the State seeks to create a more agile and accessible environment for MIPYMES, promoting their formal growth, financial inclusion, and active participation in the national economy.

► Decree No. 4638/2025 – The 69th Additional Protocol to ACE No. 35 between MERCOSUR and Chile is incorporated into the national legal system.

The Executive Branch issued Decree No. 4638/2025, incorporating into national law the 69th Additional Protocol to ACE No. 35, concluded between the States Parties of MERCOSUR and the Republic of Chile. With this measure, Paraguay updates and harmonizes its regulations on rules of origin, completely replacing Annex 13 of the ACE and its previous amendments.

The new text seeks to modernize the regulatory framework governing trade between MERCOSUR and Chile, adapting it to the current needs of operators and aligning it with international standards on trade facilitation. In this regard, more precise definitions, simplified administrative processes, and a clearer procedural structure are introduced, resulting in greater legal certainty and predictability for economic agents.

The Rules of Origin included in the Protocol establish the criteria that determine when a product can be considered originating and, therefore, benefit from the tariff preferences of the agreement. Among the main amendments are the following:

Updating of the rules of origin: The criteria under which a product is considered to be originating in MERCOSUR or Chile are specified, including the tariff jump (first four digits of the tariff nomenclature) for granting the origin regime. This tariff jump may be waived if the CIF value of non-originating materials used in the production of the goods does not exceed the respective tolerance margins of the FOB value of the finished product (40% in general and 45% for certain products).

New specific origin requirements: For certain agricultural, food, and industrial products, detailed technical requirements (such as the use of regional raw materials or specific manufacturing processes) are established that must be met in order to access the preferences of the agreement.

Recognition of digital certificates of origin: The protocol grants full legal validity to certificates issued electronically and digitally signed by authorized certifying entities. This represents a significant step toward the digitization of regional foreign trade, reducing administrative costs and time.

Strengthening of control and verification procedures: Clear rules are established on record keeping, the submission of sworn statements of origin, deadlines for verification by customs authorities, and mechanisms for cooperation between competent authorities. Verifications may even be carried out through visits to the premises of exporters or producers, under regulated conditions and with respect for the confidentiality of information.

Accumulation and flexibility mechanismsThe possibility remains for materials originating in any signatory country to the ACE to be considered as originating in the other countries. In addition, a differentiated origin regime favorable to Paraguay (50% tolerance margin) is incorporated until 2038, with the possibility of automatic renewal for successive 5-year periods, which is applicable to parts of chapters 38, 39, 61, 62, 62, 85, 87, 94, and 95 of the tariff nomenclature.

Transition and repeal of previous rulesThe new protocol repeals the previous ones (58th, 63rd, 65th, and 68th) that amended the same annex, unifying the current provisions on origin into a single text. This facilitates the practical application of the regime and eliminates inconsistencies arising from overlapping rules.

The Additional Protocol will enter into force sixty days after the Latin American Integration Association ("ALADI") notifies the signatory countries of the receipt of formal notifications of compliance with the internal procedures of each State Party. At the national level, the MIC will be the authority responsible for its implementation and coordination, together with the other public institutions competent in customs and trade matters.

With this incorporation, Paraguay reaffirms its commitment to regional economic integration, trade liberalization, and the harmonization of rules that promote a more competitive and predictable environment for businesses. The new rules of origin regime is a key tool for strengthening the country's participation in regional value chains and improving access conditions for Paraguayan products to the Chilean market and other MERCOSUR partners.

► General Resolution No. 36/2025 - Administrative measures were established for guarantee trusts.

The DNIT issued General Resolution No. 36/2025, which establishes new administrative measures applicable to guarantee trusts, with the aim of facilitating their identification and simplifying compliance with their tax obligations.

This resolution extends to all guarantee trusts the special conditions that previously only benefited those established under the "Che Róga Porã" program, thus seeking to standardize the administrative treatment of this type of fiduciary structure.

Guarantee trusts are considered transparent legal structures under Law No. 6380/2019, and therefore they usually register for Corporate Income Tax ("IRE") and Value Added Tax ("VAT") obligations. However, in practice, they only record economic movements at the beginning and end of the contract, remaining inactive for most of its term.

The DNIT seeks to reduce the operational burden involved in filing monthly returns with no movement and recording receipts. Consequently, the resolution introduces a more streamlined procedure adapted to the nature of these financial instruments. Among the main provisions are:

Registration in the Single Taxpayer Registry ("RUC”): Guarantee trusts must register only with the annual obligations of General IRE - Code No. 700 and "Annual Receipt Registry" - Code No. 956, thus eliminating the monthly administrative burden of document filing and VAT.

VAT return: These trusts will only have to settle and file VAT returns in periods when there are operational movements, eliminating the obligation to file monthly returns without activity. It will not be necessary to maintain the General VAT obligation (code 211) active in the RUC.

Adjustment of already registered trusts: Guarantee trusts that are already registered must cancel the General VAT obligation and the monthly receipt registration, replacing them with the annual registration. This transition must be accompanied by the declaration of closure of the canceled obligations, corresponding to the last fiscal period affected.

The new regime represents a significant step forward in terms of administrative simplification, as it adapts the formal requirements of the DNIT to the operational reality of guarantee trusts. These measures reduce compliance costs and times, benefiting both trustees and trustors who bear the costs of the trust business. In addition, the scheme reinforces the traceability and control of trust movements through digitized annual records, maintaining fiscal transparency without imposing unnecessary burdens.

Felicitamos a nuestros socios y cada uno de los abogados que conforman las áreas clasificadas, por este destacado logro.

Estamos muy orgullosos de este reconocimiento que destaca la dedicación de nuestro equipo, la calidad del servicio brindado y la confianza de nuestros clientes.

Legal 500 es uno de los principales rankings internacionales que se encarga de analizar firmas de abogados a nivel mundial para sus publicaciones.

On October 14, 2025, the Chamber of Deputies enacted the “Securities and Commodities Market Law” (the “Law”), previously approved by the Chamber of Senators. Consequently, the Law was sent to the Executive Branch for its promulgation. The bill had originally been submitted to Congress for consideration by the Ministry of Economy and Finance.

The Law seeks to unify the local legal framework related to the securities and commodities market, which up until now had been scattered across seven separate laws, including those establishing the Superintendency of Securities, the Securities Market Law, the law regulating investment funds, and the law governing credit rating agencies, among others.

Accordingly, the Law -as well as the Resolution regulating the Law to be issued in the coming months- will now regulate the operations of entities directly or indirectly involved in the securities market, such as stock and commodity exchanges, brokerage firms, securities depositories, investment funds, credit rating agencies, clearing and settlement houses, securitization companies, securities traders, and investment advisors.

Additionally, the Law introduces rules governing crowdfunding, which previously was not regulated as an activity.

The Law also reaffirms the Central Bank of Paraguay as the governing authority over activities related to the securities and commodities market, acting through the Superintendency of Securities. In this regard, the Superintendency of Securities will issue the corresponding resolution to regulate the provisions of the Law in the coming months.

In future updates, we will examine in greater detail the main reforms introduced by the Law, which establishes the new regulatory framework for the Securities and Commodities Market and for investment services and activities.

The Senate approved a bill to reform of the metropolitan public transport service.

Start Orders

August 26, 2025

The Ministry of Public Works and Infrastructure (“MOPC”) issued commencement orders for the construction of sanitary sewer systems in 3 cities as part of a sanitation program. Value of the project: USD 40 million.

Call for Bids

September 12, 2025

The National Directorate of Public Procurement (“DNCP”) published on its official website an International Public Tender (“LPI”) for the paving of Route PY12 (Cruce Colonia Margarita – Itakyry section), convened by the MOPC.

Bill

July 24, 2025

The Executive Branch submitted a bill to merge the Ministry of Industry and Commerce, the Vice Ministry of Mines and Energy and the National Secretariat of Tourism into the new Ministry of Industry, Commerce, Tourism, Mines and Energy.

Project Socialization

August 19, 2025

The MOPC launched the public consultation process for the tender of the project to improve urban access to Route PY01. Value of the project: USD 180 million.

Award

September 23, 2025

The MOPC announced the awarding of International Public Tender No. 3101, for the improvement and duplication of Route PY01 on the Cuatro Mojones – Quiindy section, which will demand investments estimated in over USD 400 million..

Call for Bids

September 30, 2025

National Directorate of Public Procurement (“DNCP”) published National Public Tender ID No. 475451 for the execution of maintenance dredging works on the Paraguay River along the section from the Paraná River confluence to the Apa River mouth.

More Information:

I. The Senate Approves with Amendments a Law Reforming the Metropolitan Public Transport Services

On July 24, the Executive Branch, through the Ministry of Public Works and Communications (MOPC), submitted to the National Congress the bill entitled “Establishing Oversight of Land Transportation and Amending and Expanding Provisions of Law No. 1590/2000 Relating to the Metropolitan Public Passenger Transport Service” (the “Bill”). The Bill seeks to redefine the metropolitan public transport service and, at the same time, reorganize the sector’s oversight through the creation of a modern institutional framework.

A. Institutional Framework

El Proyecto de Ley establece que la prestación de los Servicios de Transporte Público Metropolitano (“Servicios”) se organizará mediante contratos de concesión adjudicados por el MOPC a través de licitaciones públicas. Los Servicios a ser concesionados incluyen:

fleet supply contracts,

infrastructure supply contracts,

fleet operation services, and

complementary services.

Fleet supply, fleet operation, and complementary service contracts may be awarded for terms of up to 15 years, while infrastructure supply contracts may extend up to 20 years.

The Bill also allows concession contracts to include arbitration as a dispute resolution mechanism for matters of a private nature, thereby introducing higher predictability standards for international stakeholders.

B. Financing and Tariff Scheme

The Bill establish a Financing Administration Trust with segregated assets to be managed managed by the Development Finance Agency (Agencia Financiera de Desarrollo or AFD) (the “Trust”)acting as trustee and the MOPC as trustor. The Trust is aimed exclusively at ensuring timely payments to service providers. This mechanism seeks to reduce liquidity risks and enhance the system’s financial stability.

The Trust’s funds may be carried over between fiscal years and must cover firm liabilities for a minimum of 12 months, according to the contractual schedule. Revenues from the electronic ticketing system will be transferred daily to the Trust, which will in turn pay the operators as instructed by the MOPC. Additionally, internal and external audits are established, including the oversight by the Office of the Comptroller General of the Republic (CGR), to ensure transparency and proper management of resources.

Regarding fares, the Executive Branch will set user tariffs based on MOPC proposals, taking into account criteria such as : affordability, sustainability, and equity. Provider’s compensation may be calculated based on variables such as kilometers traveled, passengers transported, or fleet and infrastructure availability, as well as service levels and performance indicators. To safeguard economic balance, remuneration will be subject to automatic adjustment mechanisms through polynomial formulas linked to relevant cost evolution, thus providing long-term revenue certainty.

C. Technical and Sustainability Conditions

The Bill introduces a maximum age of 15 years for fleet units, requiring the progressive renewal of buses in service. Likewise, it also authorizes mandates for low- or zero-emission vehicles, opening space for investment in new technologies and sustainable mobility solutions.

The Bill also allows the State to acquire bus fleets and infrastructure for the service and to operate them under different contractual schemes—leasing, commodatum, usufruct, management trusts, financial leasing, or others—depending on the public interest. For electric or hybrid buses and their charging infrastructure, direct pilot agreements with specialized providers are contemplated.

A special regime is also created for assets allocated to the service, requiring registration in a dedicated registry, setting out rules for dereservation upon contract termination, and establishing protections to limit attachment or enforcement by creditors, thereby strengthening operational security .

Furthermore, the mandatory interoperability of electronic ticketing systems with multiple payment methods is introduced, encouraging technological innovation in the user experience and creating opportunities for digital service providers.

D. Guarantee of Service Continuity

From the users’ perspective, the Bill guarantees continuous provision of the service even in the event of strike , by establishing minimum coverage percentages. It also reinforces users’ rights through the establishment of quick and accessible complaint mechanisms and granting the regulator broad supervisory powers to ensure the quality and safety of the service.

E. Legislative Process

The Bill was approved by the Senate, the chamber of origin, on September 9, 2025, and is currently pending before the Chamber of Deputies for its second constitutional review. The Bill is available at the following link.

II. Progress of the Sanitation Program for Intermediate Cities

MOPC recently issued commencementorders for the construction of sanitary sewer systems in 3 of the 4 cities included in the Sanitation Program for Intermediate Cities (the “Program”), financed by the Development Bank of Latin America and the Caribbean (CAF). The cities are: Santa Rita (Alto Paraná), San Ignacio Guazú (Misiones), and Carapeguá (Paraguarí).

The Program aims to expand sewer network coverage, optimize wastewater treatment, and improve the drinking water supply. The Program also encompasses the construction of collection networks, pumping stations, household connections, and wastewater treatment plants (WWTPs), enabling effluents to be returned to the environment under safe and sustainable conditions. More than 120,000 people in the four selected cities are expected to benefit.

The contracts for the works were awarded through International Public Tender No. 33/24 for a total value of approximately ₲ 358,937 million (approximately USD 50 million), to the following companies:

In Santa Rita, to Construcciones y Viviendas Paraguayas S.A. (COVIPA) with an investment of ₲ 82,459 million (approximately USD 11.5 million).

In San Ignacio Guazú, to the Rovella-TOCSA Consortium, with an investment of ₲ 114,423 million (approximately USD 16 million).

In Carapeguá, to the Carapeguá Sanitation Consortium. The investment will amount to ₲ 87,004 million (approximately USD 12 million).

The execution of the works will be overseen by the Directorate of Drinking Water and Sanitation (DAPSAN), a division of the MOPC. Completion and delivery are scheduled for July 2028.

The Project marks a significant step in strengthening tParaguay’s sanitation infrastructure, not only by expanding coverage in intermediate cities facing growing urban demand, but also by creating opportunities for the private sector in areas such as engineering, construction, equipment supply, and the operation of related services.

III. Tender for the Paving of Route PY21: Cruce Colonia Margarita – Itakyry Section

General Aspects

On September 12, 2025, MOPC, through the National Directorate of Public Procurement (DNCP), published International Public Tender No. 468137 corresponding to MOPC Call No. 94/2025 (the “Project”). The Project involves the asphalt paving of a 26.5 km section of Route PY21, which connects Cruce Colonia Margarita with the city of Itakyry, in the department of Alto Paraná.

The Project is designed to facilitate the transportation of goods along this corridor while improving access to healthcare and educational centers.

Characteristics

Project Value and Financing The works are estimated at ₲ 134,280,210,326 (approximately USD 19 million). Financing will be provided through a loan from the Development Bank of Latin America and the Caribbean (CAF), approved under Law 6897/2022. An advance payment of 10% of the contract is foreseen, and the validity will extend until the final acceptance of the works.

Bid Maintenance Guarantee Bidders are required to submit a bid maintenance guarantee equivalent to 5% of the bid amount, either through a bond or a bank guarantee.

Awarding System The contract will be awarded be based on the lowest economically advantageous offer, provided that it complies with the substantial conditions of the bidding documents.

Subcontracting Subcontracting is permitted; however, subcontracted works may not exceed 20% of the total contract amount.

Contracting Authority MOPC.

Relevant Dates Key dates in the process are as follows: (i) October 13, 2025, as the deadline for submitting questions;

(ii) October 17, 2025, for the submission of bids (09:00 a.m.) and their opening (09:30 a.m.) in the Assembly Hall of the MOPC Central Building.

Through this tender, the MOPC continues to advance the consolidation of Route PY21 as a strategic corridor for agricultural production, strengthening market access and contributing to the development of local communities.

IV. Executive Branch submits Bill to create the Ministry of Industry, Commerce, Tourism, Mining and Energy

On July 24, the Executive Branch submitted to the National Congress the bill entitled “To Creat the Ministry of Industry, Commerce, Tourism, Mining and Energy” (the “Bill”), which seeks to merge and reorganize various areas of the Executive into a single ministry with expanded powers over industrial, energy, mining, and tourism matters.

Institutional Framework

The Bill provides for absorbing the Ministry of Industry and Commerce, the Vice Ministry of Mines and Energy (currently under the MOPC), and the National Secretariat of Tourism. Consequently, the new ministry would be organized into 5 vice ministries: Industry; Commerce and Services; MSMEs; Tourism; and Mines and Energy.

Article 7 of the Bill sets out its functions and powers, which include formulating national policies in industrial, commercial, energy, mining, and tourism; issuing regulations and technical guidelines; and representing the State before autonomous entities in the sector.

Powers in the Energy Sector

The new ministry will assume, among others, the following responsibilities:

Formulate national energy and mining policy.

Establish technical guidelines for the management of energy and mineral resources.

Grant authorizations, permits, licenses, approvals, contracts, and concessions.

Regulate, oversee, and supervise activities related to energy, mining, and hydrocarbons.

Implement policies to ensure energy security, including the expansion of electricity generation from different sources.

These provisions would integrated into the current regulatory framework, which includes, among others, Law 966/64 (Organic Charter of ANDE) and Law 6977/22 (Promotion of Non-Conventional Renewable Energies, currently under amendment)1. If enacted as originally drafted, certain powers currently vested in ANDE under Law 966/64 would be transferred to the new ministry.

Cross-Cutting Scope

Beyond its powers in the energy sector, the ministry would be empowered to promote national industry, foster exports, regulate quality standards, encourage technological innovation, and develop policies for cultural and ecological tourism. It may also establish fees for administrative services and participate in international negotiations related to trade, energy, and mining.

Legislative Process

The Bill is currently under consideration in the Chamber of Deputies. It has already received opinions from the Committees on Economic and Financial Affairs, Budget Execution Control, Legislation and Codification, and Energy and Mining. Its discussion, originally scheduled for the plenary session on September 16, 2025, was postponed. The full text is available at the following link.

V. MOPC moves forward with public call process for the Urban Access to Route PY02 Expansion Project

In August, the MOPC held informative sessions to present the project to expand of the Urban Access to Route PY02, a strategic initiative designed to improve connectivity between Greater Asunción and cities in the country’s interior.

The project includes the construction of an elevated urban highway stretching nearly 4 kilometers, with two roadways and four lanes, connecting Ñu Guasú and Silvio Pettirossi avenues, complemented by two new access corridors to Route PY02.

The first, the so called Ypacaraí – Areguá – Luque Corridor, starting at km 41 of Route PY02 and including a new bypass in Areguá, designed to streamline traffic and boost local trade and tourism.

The second, the Ypacaraí – San Bernardino – Luque (Tarumandy) Corridor, beginning at km 43 and including lane duplication, urban improvements, and direct access to Nueva Colombia and Route PY02 itself.

The works will be executed by Rutas del Este S.A., the Route PY02 concessionaire under a Public-Private Partnership (PPP) scheme, with an estimated investment of USD 180 million. The project is currently in the public call process for competitive subcontracting of the works.

This project not only seeks to significantly reduce travel times between Greater Asunción and the country’s interior cities, but also to generate positive impacts on road safety, regional tourism, and economic competitiveness, consolidating itself as one of the most important urban interventions in Paraguay’s road infrastructure.

VI. MOPC awards the International Public Tender for the duplication of Route PY01

On September 23, the MOPC announced the award of International Public Tender No. 3101 (the “Tender”) for the improvement and duplication of Route PY01, along the 108-kilometer section between Cuatro Mojones and Quiindy (the “Project”). The Project will be executed under the Public-Private Partnership model, in accordance with Law No. 5102/13 and Regulatory Decree No. 1467/2024.

The award was granted to the consortium Rutas del Mercosur (the “Consortium”), composed of Tecnoedil S.A. (a Paraguayan company), Alya Constructora S.A. (a Brazilian company), Construpar S.A. (a Paraguayan company) and Semisa Infraestructura S.A. (an Argentine company).

The proposal submitted by the Consortium includes a Deferred Investment Payment of USD 24,077,936.70 (VAT included), which represents an 8% reduction compared to the reference value set forth by the MOPC, within a total investment project exceeding USD 400,000,000.

The initiative covers the duplication of Route PY01 from Cuatro Mojones, in the Central Department, to the city of Quiindy, in Paraguarí, spanning a total of 108 kilometers, with maintenance for 30 years.

This is the second project implemented under the Public-Private Partnership (PPP) model in the country and includes overpasses, bypasses and service roads that will enhance mobility, boost development, and reduce travel times for thousands of users. With this Project, which represents one of the most significant urban interventions in the country’s road infrastructure, Paraguay takes another step towards the modernization of its road network and strengthens its role as a logistics hub in the region.

VII. Call for bids for maintenance dredging of the Paraguay River

On September 30, 2025, the National Directorate of Public Procurement (DNCP) published National Public Tender ID No. 475451 (“Tender”), corresponding to MOPC Call No. 108/2025, convened by the Ministry of Public Works and Communications (MOPC), for the execution of maintenance dredging works on the Paraguay River along the section from the Paraná River confluence to the Apa River mouth.

The reference value of the contract amounts to ₲ 475,098,391,960 (approximately USD 63 million), with a contract term of 36 months from the notice to proceed. The bidding process is supported by a budget availability certificate issued by the Ministry of Economy and Finance.

Scope of works The Tender is divided into 3 lots, each comprising 3 main items:

Dredging of critical navigation steps (89 in total; number subject to modifications).

Supply and installation of between 36 and 50 buoys and AIS-equipped beacons per lot, including their mooring systems and full maintenance for the 36-month contract term.

Specialized maintenance and supervision services, including surveys, inspections, and technical assistance.

The works must ensure navigability for design convoys up to 290 m in length and 65 m in beam, guaranteeing a minimum draft of 3.05 m (10 feet) plus a 0.30 m under-keel safety margin.

Key dates

October 15, 2025: deadline for questions.

October 21, 2025: submission and opening of bids.

Strategic relevance

The tendered section constitutes the country’s main inland waterway. With this intervention, the MOPC seeks to ensure the continuous operability of the Paraguayan waterway, which is essential for foreign trade and regional cargo transport.

For more information on the tender, please click on the following link: ID 475451

Infrastructure Pipeline

Our team provides access to the Infrastructure Pipeline, an updated tool that offers a clear and organized overview of the most relevant projects in the sector. Available .

Vaporizers and nicotine-free essences are included in the category of cigarettes and tobacco products subject to the Selective Consumption Tax ("ISC"), and the minimum tax rate limit for those products is increased.

General Resolution No. 35

July 24, 2025

The National Tax Revenue Directorate (“DNIT”) extended the deadlines for registration in the Registry of Persons Linked to Customs Activities (“PVAA”).

2026 National General Budget Bill

August 25, 2025

The Executive Branch submitted the draft General National Budget for 2026 ("PGN") to Congress.

Binding Consultation No. 712

August 2025

Extension of the useful life of biological assets in plantations.

Binding Consultation No. 709

July 2025

Aspects related to electronic bills of exchange.

Binding Consultation No. 694

May 2025

Tax treatment of refunds made by the parent company abroad.

Binding Consultation No. 678

April 2025

Limitation on the deductibility of self-assigned remuneration of the owner of a sole proprietorship.

August – 2025:

► Law No. 7508/2025 – Inclusion of nicotine-free vapes and essences in the category of cigarettes and tobacco products, and increase in the minimum ISC rate for those products.

The Executive Branch enacted and published Law No. 7508/2025 in the Official Gazette, establishing health measures related to Electronic Nicotine Delivery Systems (“ENDS”), Similar Non-Nicotine Delivery Systems (“SNDS”), and other similar devices, commonly referred to as vapes, vaporizers, or electronic cigarettes. These measures include a tax measure consisting of the inclusion of (1) vaping devices and (2) their vaporizable liquids, with and without nicotine, in the category of cigarettes or tobacco products taxed by the ISC, whereas previously only tobacco products used in vaping devices were taxed.

In addition, the minimum rate for vaping devices and their essences was also increased from 18% to 22%, thus restricting the Executive Branch's power to reduce the ISC rate for these goods, while keeping it intact for other products in the same category, such as cigarettes, tobacco, etc. In practice, this will not have an im y impact, as the rate for all products in this category has already been set at 22% by Decree No. 8878/2023.

What would have an immediate impact is the new ISC tax on imports of vaping devices without essences and nicotine-free essences for vaping devices, to which a 22% surcharge is immediately added. This is an issue that importers in this sector, in particular, should pay close attention to and consider in their day-to-day operations.

► General Resolution No. 35/2025 – Extension of the validity periods for registrations in the PVAA registry.

The DNIT issued General Resolution No. 35/2025, introducing adjustments to the regulations governing the authorization, renewal, and updating of PVAA. The measure complements the provisions of General Resolution No. 30/2025 regarding the validity of registrations for importers and customs brokers.

Now, registrations for regular importers, aircraft maintenance and repair companies, and duty-free shops valid as of March 1, 2025, will be extended until October 31, 2025, rather than August 31, 2025, as initially planned. Thus, the deadline for completing this procedure before these registrations expire has been extended from one to three months. For other types of PVAA, registration remains valid until May 31, 2026, with one month to complete the procedure.

An interesting feature of the new mandatory registration schedule for the PVAA registry is that the categories of "Occasional Importer" and "Diplomats" have been eliminated, which means that registrations in these categories would not be affected by the previously indicated expiration dates, although the obligation to begin the renewal process as of August 1, 2025, remains in effect.

The resolution also provides for the possibility of the General Customs Administration authorizing exceptional treatment in duly justified cases, allowing for the partial submission of requirements without interrupting essential foreign trade operations. With these modifications, the DNIT seeks to provide greater predictability to international trade actors, while ensuring the collection of taxes and the continuity of customs operations.

► The Executive Branch sent the PGN for 2026 to Congress.

On August 25, 2025, the Executive Branch presented the General National Budget for 2026 (the "PGN") to Congress, which will be reviewed for approval. Revenues are estimated at PYG 149.17 trillion (USD 20.896 billion), while the estimated fiscal deficit for fiscal year 2026 stands at 1.5% of GDP for the Central Administration, thus returning to compliance with the limits established in Law No. 5098/2016 on fiscal responsibility.

The Executive's Message adds that the tax burden would be 11.6% of GDP and tax collection would grow by 8% compared to 2025. Real GDP growth in 2026 is projected at 3.8%. No changes or eliminations of exemptions are expected, meaning that tax policy will remain stable in 2026.

The PGN bill sets limits on bonuses and prohibits gratuities, except for officials of the National Tax Revenue Directorate (DNIT). It also provides for the obligation to use the National Development Bank (BNF) for inter-institutional payments and compensation without affecting tax revenues.

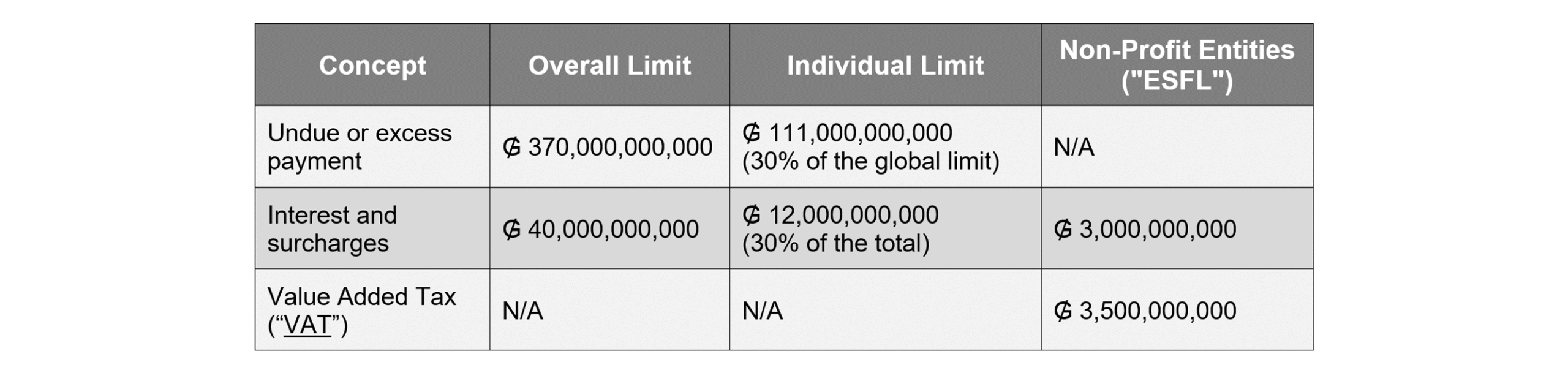

The PGN also provides for tax measures, one of which is annual budget limits for crediting taxpayers with the balances due to them for (1) undue or excess payments and (2) legal accessories. This is a budgetary measure that has been implemented every year since Law No. 5061/2013 (see Article 7) and Decree No. 850/2013. For fiscal year 2026, the PGN bill establishes the following overall and individual (per taxpayer) budget limits:

The overall limits represent the maximum amount that the DNIT can credit for the items indicated throughout the 2026 fiscal year, while the individual limits per taxpayer are 30% of the overall limit for each item. This means that no taxpayer can represent a percentage of credits greater than that indicated, thus preventing one taxpayer from excluding the others.

These budget limits do not apply to VAT refunds to ESFLs as a result of court rulings, as these have their own limits. In addition, the way in which this item is credited to ESFLs also differs from the normal regime, as these amounts are paid in cash and not credited to the taxpayer's tax account, as is the case in other instances.

If the total budget limits are reached during the fiscal year, the amounts pending credit are deferred to the following fiscal year without generating legal accessories. The area responsible for making the credits must correlatively record the resolutions that provide for them, for inclusion in the PGN for the following fiscal year.

► Binding Consultation No. 712 – Extension of the useful life of biological assets in plantations

The DNIT was consulted regarding the possibility of extending the useful life of the Neem tree plantations that make up a company's fixed assets, with the aim of starting their depreciation in 2024, extending the depreciation period to 20 years from then on, and recognizing this expense as deductible in the determination of the IRE.

In its ruling, the DNIT decided to authorize the requested extension, establishing that the plantations in question may be depreciated over a period of 20 years. It also ruled that the depreciation from these assets will be deductible for income tax purposes starting in fiscal year 2025, although, unfortunately, it did not elaborate further on the start date of the depreciation of the plantations, which, according to Article 30, paragraph 2, of the annex to Decree No. 3182/2019, is from the first harvest or cut.

The decision is based on the powers provided for in the last paragraph of Article 31 of the Annex to Decree No. 3182/2019, which allows the DNIT to set a useful life other than that specified in the regulations when supported by a technical report.

The resolution highlights that the useful life of biological assets is directly linked to the calculation of depreciation, which requires determining both the period of use and the residual value of the asset. In this case, the firm provided technical reports demonstrating that the cultivated species has a useful life of 20 years, exceeding the 5 years originally provided for in the regulations.

The DNIT specified that the authorization is limited exclusively to the assets identified in the application and is not extendable to other similar assets that have not been subject to technical analysis. Finally, it recalled that, in order to be deductible, depreciation must comply with the general requirements established in Article 14 of Law No. 6380/2019: it must be necessary to maintain the source of production, represent an actual expenditure, be properly documented, and be in line with market value.

This ruling confirms the importance of technically supporting any request to modify the useful life of depreciable or amortizable assets, especially in the case of biological assets whose productivity may vary depending on operating conditions.

► Binding Consultation No. 709 – Aspects relating to electronic bills of exchange.

In a recent binding consultation, the DNIT was asked whether it was possible to incorporate the fields provided for in Law No. 6542/2020 on bills of exchange into the electronic invoice format in order to guarantee the validity of such documents as enforceable instruments in the event of legal collection.

In addressing this issue, the DNIT distinguished between information on the exchange invoice that is validated by the Integrated National Electronic Invoicing System ("SIFEN") and information that is not, the former being either mandatory or optional. It is this validatable information that is sent to the SIFEN, as provided for in the current technical documentation. Consequently, any electronic invoice that includes bill of exchange information that differs from that provided for in the technical documentation will not be approved by the system.

The current version of the SIFEN technical documentation strictly establishes the fields that can be included, and these do not include those relating to the assigned debt, as required by Law No. 6542/2020. However, the regulations do allow space on the electronic invoice for the inclusion of additional information from the issuer (field J003, up to 5,000 characters in length), in which any other information that the issuer deems relevant may be included, such as that required by Law No. 6542/2020.

This data may appear in the electronic document or in its graphic representation (“KuDE”) sent to the customer, but it is not included in the XML file sent to SIFEN for validation, nor will it form part of the electronic tax document approved by SIFEN. In summary, taxpayers seeking to issue exchange invoices must take into account the distinctions made between validatable and non-validatable information for the purposes of including the relevant information.

► Binding Consultation No. 694 – Tax treatment of refunds made by the parent company abroad.

The DNIT issued a ruling on the tax treatment applicable to reimbursements received from its parent company in Spain. The operation consisted of the branch in Paraguay advancing certain expenses—such as hiring personnel, market studies, and technical support—which were subsequently reimbursed by the parent company under a contract called a "transitional mandate." The company understood that these amounts did not constitute taxable income and, consequently, should not be subject to VAT, Corporate Income Tax ("IRE"), or Non-Resident Income Tax ("INR").

The DNIT concluded that the reimbursements in question did not correspond to a mandate contract, but rather to the provision of services, which meant that they were subject to the local tax regime. In particular, it determined that:

The transactions must be framed within the Special Rules for the Valuation of Transactions, given the nature of related parties.

The agreed profit margin will be subject to INR, although it should have referred to IRE, since this margin would belong to the local branch.

The amounts paid by the parent company to the branch are subject to VAT, as they constitute services used in Paraguayan territory.

Payments to suppliers in Brazil will be subject to INR and VAT when the services are used or exploited in Paraguay and are linked to income taxed by the IRE.

To reach this conclusion, the DNIT examined the contract submitted, which expressly defined the relationship as a provision of services aimed at market opening, technical support, and administrative management in Paraguay and Brazil. In view of this, it considered that this was not a mere reimbursement under mandate, but rather a scheme of services provided to the foreign parent company.

The DNIT also pointed out that, as the parties were related, the transaction had to comply with the principle of independence set out in Law No. 6380/2019, so that the prices and conditions were comparable to those that would have been agreed by independent parties in similar circumstances. Finally, it insisted that the documentation must accurately reflect the concepts of "reimbursement" and the corresponding expenses in order to adequately support the accounting and settlement of taxes.

With this ruling, the DNIT sets an important precedent: reimbursements from the parent company to the local establishment, when related to the provision of services, are subject to IRE, INR, and VAT under the conditions indicated.

► Binding Consultation No. 678 – Limitation on the deductibility of self-assigned remuneration of the owner of a sole proprietorship.

The DNIT has issued a response to a binding consultation addressing the deductibility of self-assigned remuneration by the owner of a sole proprietorship, in their capacity as a taxpayer of the IRE and Personal Income Tax ("IRP"). The consultant wanted to know whether, when paying IRP on his remuneration as the owner of the sole proprietorship, this was deductible only up to 1% of gross income on the General IRE form.

The DNIT concluded that the deductibility of self-assigned remuneration in the IRE depends on the type of service provided by the owner:

100% deductibility: If the remuneration is received for independent personal services, the entire amount is deductible in the IRE. This deduction applies as long as the service provider (a) is an IRP or INR taxpayer, and (b) is not considered "senior staff" of the company.

Deductibility limited to 1% of gross income: If the remuneration is received as senior personnel, the deduction will be limited to 1% of the company's gross income for the fiscal year, regardless of whether or not the owner is an IRP taxpayer, which allows for greater flexibility than that provided for in the regulations.

In this regard, the DNIT clarified that the total deduction (100%) for independent personal services applies if the owner, partner, or shareholder, who is an IRP or INR taxpayer, receives remuneration for the provision of such services to himself in his capacity as a sole proprietor, which must be duly documented by means of a contract and a sales receipt to justify the total deductibility. In this way, the DNIT seems to be indicating that this would be possible if a person contracts with themselves for services other than those of the senior staff of the sole proprietorship.

El Ministerio de Trabajo, Empleo y Seguridad Social (MTESS) dictó la Resolución Nº 976/2025, mediante la cual se aprueba un nuevo reglamento para la homologación y registro del Reglamento Interno de Trabajo (RIT). Esta resolución entra en vigor el 1 de octubre de 2025 y deja sin efecto la Resolución N.º 1342/2020.

Con esta medida, el MTESS busca actualizar y modernizar el proceso, incorporando protocolos de prevención de la violencia laboral y digitalizando la tramitación para dotar de mayor agilidad y seguridad al sistema.

Key Developments introduced by Law 7452

Duración

El RIT tendrá una vigencia máxima de cinco años. Esto implica que las empresas deberán renovar periódicamente el reglamento, revisando y actualizando sus disposiciones conforme a los cambios normativos y a las necesidades organizacionales.

Contenido obligatorio

Además de lo previsto en el Código del Trabajo, el reglamento debe incluir protocolos para la prevención, investigación y sanción de la violencia y el acoso laboral, en cualquiera de sus formas: física, sexual, psicológica o de otra índole. También deberá incorporar mecanismos de resolución de conflictos, lo que coloca a las empresas en un rol más activo en la promoción de un clima laboral sano, seguro y respetuoso.

Documentación

Para iniciar el trámite, las empresas deberán presentar el reglamento en formato PDF y en formato editable, firmado por representantes del empleador y de los trabajadores. Adicionalmente, se exige la declaración jurada de los representantes de los trabajadores, conforme al modelo aprobado en la resolución. En el caso de que el documento sea firmado por sindicatos, el MTESS verificará la vigencia de los mandatos para garantizar la legitimidad de la representación.

Procedimiento digitalizado

El trámite será gestionado a través del Sistema REOP, con expedientes electrónicos en el Sistema VIRTU. Esto permitirá un proceso más ágil y transparente. El procedimiento incluye la generación de la boleta de pago del arancel, la carga de la documentación y la posibilidad de dar seguimiento al estado de la solicitud, que podrá encontrarse en trámite, aprobado, denegado o archivado.

Plazos

El MTESS contará con un máximo de quince días hábiles para dictar resolución desde la emisión del último informe técnico. Por su parte, los solicitantes dispondrán de diez días hábiles para subsanar las observaciones que eventualmente se formulen. La omisión de respuesta en ese plazo implicará el archivo automático del expediente, lo que obliga a las empresas a mantener un estricto control de los plazos procesales.

Publicación interna

Una vez homologado, el RIT deberá ponerse a disposición de los trabajadores. Esto podrá hacerse fijando el documento en lugares visibles del establecimiento o distribuyéndolo de forma digital, siempre incluyendo el número y la fecha de la resolución que lo homologó. Los empleadores deberán además entregar copia a los nuevos trabajadores que ingresen después de la aprobación.

Arancel

Se establece un costo fijo para el trámite, equivalente a un jornal mínimo para actividades diversas no especificadas, el cual deberá abonarse a través de la red bancaria.

Expedientes en Trámite

Los expedientes iniciados antes de agosto de 2024 serán dados de baja automáticamente, salvo que el recurrente presente un reclamo dentro de los noventa días siguientes a la entrada en vigencia de la resolución. Por otro lado, los expedientes iniciados a partir de agosto de 2024 continuarán su curso conforme al procedimiento que regía en el momento de su presentación.

Entrada en Vigencia

La Resolución N.º 976/2025 comenzará a regir el 1 de octubre de 2025. A partir de esa fecha, todas las solicitudes deberán ajustarse al nuevo procedimiento establecido por el MTESS.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

Está vigente la Ley N.º 7534/2025, que modifica y amplía los artículos 2 y 11 de la Ley N.º 5508/2015, a su vez modificada por la Ley N.º 6453/2019, y deroga la Ley N.º 5344/2014 sobre reposo por maternidad en cargos electivos.

Principales Cambios

Ámbito de Aplicación

Se amplía la cobertura de la ley a todas las personas que trabajen en modalidad laboral bajo régimen público, privado o mixto, incluyendo:

Poder Judicial (Ley 879/81).

Trabajadores regidos por el Código del Trabajo (Ley 213/93).Ministerio Público (Ley 1562/2000).Función Pública y Servicio Civil (Ley 7445/2025).

Defensa Pública (Ley 4423/2011).

Se extiende también a cargos electivos, gobernaciones, municipalidades, banca pública, Fuerzas Armadas, Policía Nacional, entes autónomos y autárquicos.

Incluye además a instituciones de educación superior (Ley 4995/2013).

Se establece como principio rector la interpretación conforme al interés superior del niño.

Permiso de Maternidad

Duración general: 18 semanas ininterrumpidas, con certificado médico del IPS o MSPBS.

Supuestos especiales:

Parto prematuro (antes de la semana 35), bajo peso (< 2.000 grs.) o enfermedades congénitas → 24 semanas.

Embarazos múltiples → Se agrega 1 mes por cada hijo a partir del segundo.

Concurrencia de supuestos → Aplica el plazo mayor.

Fallecimiento de la madre → El permiso se transfiere al padre o cuidador designado exclusivamente para el cuidado del niño.

Prohibición: Durante el usufructo del permiso la madre no puede realizar ningún trabajo ni servicio parcial u ocasional.

Cargos electivos: derecho a 18 semanas con percepción de salario, tramitado según las disposiciones de la institución. El permiso cesa automáticamente con el reintegro de la titular.

Derogación

Se deroga expresamente la Ley N.º 5344/2014, que establecía el reposo por maternidad en cargos electivos.

Implicancias prácticas

Unificación del régimen de maternidad también para cargos electivos (ya no se aplica la Ley 5344).

Extensión clara de cobertura a sectores como Fuerzas Armadas, Policía Nacional, banca pública y entes autónomos.

Mayor certeza normativa para instituciones educativas de nivel superior.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

We are pleased to announce that Vouga Abogados advised Atlas AFPISA, the fund management company of Banco Atlas S.A., on the structuring of the Atlas I Real Estate Investment Fund, including the drafting and approval of its internal regulations before the Securities Supervisory Authority, as well as the preparation of contracts and other documents necessary for its proper implementation.

The Atlas I Real Estate Investment Fund represents a strategic and innovative initiative in the Paraguayan investment fund market, aimed at creating value for investors through a solid model with a long-term vision.

The CEO of Atlas AFPISA, Gustavo Rivas, stated:

“The Atlas I Real Estate Investment Fund is a financial instrument designed to combine capital growth and asset diversification, with a strategic focus on urban development. It represents a unique opportunity to access high-potential investments in underdeveloped sectors, under a professional and transparent management approach.”

The Vouga Abogados team involved in the transaction was led by partner Cynthia Fatecha.

El Ministerio de Trabajo, Empleo y Seguridad Social (MTESS) emitió la Resolución Nº 915/2025, por la cual se modifican artículos del Anexo N° 2 de la Resolución MTESS N° 991/2024, de fecha 17 de octubre de 2024, que aprueba el reglamento para la inscripción patronal en el Registro Obrero Patronal del Ministerio de Trabajo, Empleo y Seguridad Social y el reglamento para las comunicaciones establecidas en el Capítulo II del Anexo al Decreto N° 1989/2024. Esta resolución introduce cambios importantes a la Resolución Nº 991/2024 sobre la inscripción patronal y las comunicaciones en el Registro Obrero Patronal (REOP).

Principales modificaciones

Entrada de trabajadores no dependientes

La comunicación de entrada de trabajadores independientes, extranjeros temporales, tercerizados, contratistas, subcontratistas y cooperativas de trabajo asociado será voluntaria hasta que exista una regulación específica.

Se entenderá como prestación habitual aquella de al menos 16 horas semanales o 64 mensuales, durante más de 60 días.

La comunicación voluntaria deberá realizarse mediante la planilla de personal no dependiente del sistema REOP. Esta voluntariedad se mantendrá hasta que se emita un acto administrativo que regule específicamente el tema.

Salida de trabajadores no dependientes

Si la empresa optó por comunicar la entrada, la comunicación de salida será obligatoria y deberá registrarse en la planilla de personal no dependiente.

Plazo para comunicar el pago de aguinaldo

Se amplía el plazo: podrá comunicarse hasta los primeros 10 días hábiles del año siguiente al pago.

Exoneración de aranceles del costo del Certificado Laboral

Los empleadores que mantengan actualizada la planilla de personal no dependiente estarán exonerados del costo del Certificado Laboral

No aplicación de multas

Mientras rija la voluntariedad de la comunicación de entradas, no se aplicarán sanciones por comunicaciones tardías de entrada y salida de los casos citados en esta resolución.

Implicancias prácticas

Los empleadores tienen un incentivo económico (exoneración de arancel correspondiente al Certificado Laboral) para comunicar voluntariamente estos datos.

La medida introduce flexibilidad y busca una implementación gradual para las empresas.

Es fundamental actualizar procesos internos y verificar las planillas en el sistema REOP.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.