Executive Summary:

| Regulation | Content | Date |

| Law No. 6380 | Limit for Value Added Tax ("VAT") withholding on account for local suppliers becomes effective. | September 25, 2019 (Update) |

| Decree No. 8612 | The real estate tax values for the real estate tax and its additions, corresponding to fiscal year 2023, are fixed. | December 27, 2022 |

| Decree No. 3108 | The percentage of guarantees to be presented for the accelerated VAT refund system is fixed for 2023. | December 19, 2019 (Update) |

| General Resolution No. 105 | The SET established the schedule of due dates for taxpayers to compulsorily adhere to the Integrated National Electronic Invoicing System ("SIFEN") - Reminder for Group 3 and following. | December 17, 2021 (Reminder) |

More information:

► Law No. 6.380/2019 - Limit on VAT withholdings for local suppliers who are VAT taxpayers (UPDATE)

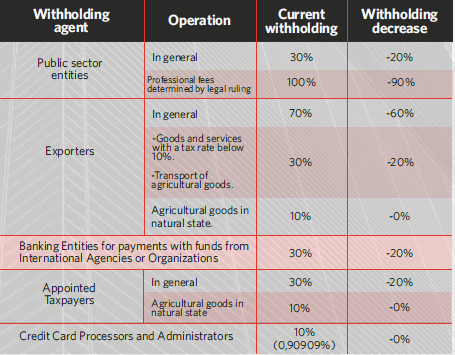

Law No. 6,380/2019 (the "Tax Law") introduced several short and medium-term novelties to the national tax regime, in respect of which its implementation is just beginning or is still pending. One of them was the limit of VAT withholdings on account, provided for in the first paragraph of Article 136. This limit was set at 10% of the tax stated in the sales receipt

The Tax Law provided for the application of such limit from the fourth year of its effectiveness, and because this provision came into effect on January 1, 2020, its implementation date was January 1, 2023. In other words, the application of this withholding limit was deferred from 2020 to 2023.

This decrease in the withholding percentage has great consequences for taxpayers that are VAT withholding agents since they must adjust their systems to the new limit. Among such taxpayers are the following:

In addition to the withholding limit, the second paragraph of article 136 of the Tax Law provided for the progressive reduction of the percentage of VAT withholding on account as from the year following the effective date of the Tax Law and until the deadline for applying the withholding limit is met, i.e., from 2021 to 2022.

However, this progressive reduction was conditioned to the issuance of a decree of the Executive Power providing the schedule for such purpose. Still, since this did not happen, it still needs to be complied with. Moreover, in Article 275 of Law No. 6873/2022, which approved the national budget for 2022, this reduction was suspended for that year, which, curiously, was replicated again for 2023 with Article 287 of Law No. 7050/2023, which approves the national budget for that fiscal year.

The inclusion of this suspension in the national budget law for 2023 appears as an error that may generate confusion among individuals since it refers to a rule that is no longer in force for that year because the progressive decrease was a transitory provision that could only be implemented from 2021 to 2022, but no longer in 2023, since from then on it makes sense because the withholding limit applies.

It would be appropriate for the SET to clarify the confusion that could be generated due to the suspension referred to above.

► Decree No. 8.612/2022 - The real estate tax rates for the real estate tax and its additional taxes are set for the fiscal year 2023.

Through Decree No. 8,612/2022 (the "Decree"), the Executive Branch fixed the real estate tax values established by the National Cadastre Service ("SNC") of the Ministry of Finance, which will serve as the taxable base for the determination of the real estate tax and its additions for the fiscal year 2023.

The amount of the tax is determined by applying the corresponding rates (normally 1%) on the tax valuation of the real estate established by the National Cadastre Service (taxable base), which is made up as follows:

- Urban real estate: land value (m2 of the property per ₲/m2) plus built value (m2 of the buildings per ₲/m2). The ₲/m2 is determined by the type of street pavement (frontage) for the land value and the construction category for the buildings.

- Rural properties: Land value (hectare ("ha") of the property per ₲/ha). The tax valuation of each district is determined according to its opportunity cost (distances to urban centers and accessibility) and the predominant type of soil according to the categories indicated in the Decree.

The tax valuation of real estate is adjusted annually according to the variation suffered by the Consumer Price Index ("CPI"), in the twelve months before November 1 of each calendar year in which such adjustment is made, as reported by the Central Bank of Paraguay. The Executive Power may make an extraordinary readjustment every five years, according to the variation in real estate value.

In that sense, the Central Bank of Paraguay informed that the variation of the CPI in the twelve months before November 1, 2022, reached 8.1%, so the Decree increased in such proportion the tax valuations for 2023. This variation can be seen for urban properties in Annex I of the Decree and rural properties in Annex II in the version of Decree No. 8736/2023.

The Decree also provides for, among other things: the valuation of properties that change from urban to rural and vice versa, the procedure for the 50% exemption for rural properties with forest priority or real right of forest surface, and the discount for rural properties with low productive areas that differ from the type of soil of their district.

► Decree No. 3,108/2019 - The percentage of guarantees to be submitted for the accelerated VAT refund regime is fixed for 2023 (UPDATE).

Article 102 of Law No. 6,380/2019 (the "Tax Law") provided that exporters and freight forwarders may request the accelerated refund of the VAT credit affected to their export or export freight operations by submitting for such purpose a bank guarantee, financial guarantee or insurance policy with a minimum validity of 90 business days from the date on which the refund request is submitted.

For the first three refund requests under the accelerated regime, the guarantee must cover 100% of the capital of the VAT credit required to SET, plus accessories. From the fourth request onwards, the guarantee must only cover the portion of the VAT credit resulting from the average percentage of rejected credits ("PCR") under the accelerated regime from January to November of the previous year, plus accessories.

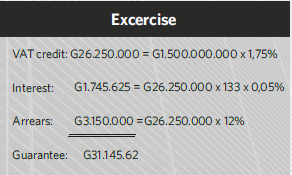

To establish the value of the guarantee, the applicant must multiply the PCR by the VAT credit for which a refund is requested. The following legal accessories must be added to the resulting amount, calculated up to the guarantee's expiration date on the amount of the VAT credit resulting from the PCR: daily interest of 0.05% and late payment penalty of 12%.

SET publishes the PCR annually, and on this occasion published that it is 1.75% for 2023, to which it attached the following example of calculation for the guarantee:

| Data | Securities |

| Amount requested: | ₲1,500,000,000 |

| Date of the request | 05/01/2023 |

| Warranty issued: | 05/01/2023 |

| Warranty expires: | 18/05/2023 |

| PCR: | 1,75% |

A more direct way of expressing the total coverage of the guarantee as a percentage of the VAT credit is achieved by expressing the accessories as percentages of the PCR. This is achieved by estimating the interest at 6.65% (133 days times 0.05%) and the late payment penalty at 12%, which, when added together, amount to 19.65% of the PCR, which can be rounded up to 20%. To add this percentage directly to the PCR, it must be expressed as 1.20 times the PCR, which for a PCR of 1.75% means a total guarantee of 2.1% of the VAT credit.

In the cases in which the bank, financial or insurance policy guarantee is lower than the amount rejected, the taxpayer must immediately pay the difference in favor of the Treasury, plus the legal accessories that will be calculated until the total payment.

General Resolution No. 105/2021 - The mandatory calendar for taxpayers to adhere to the SIFEN (REMINDER) was established.

All taxpayers, especially those in Group 3 of the SIFEN, are reminded that the SET issued General Resolution No. 105/2021 (the "RG"), dated December 17, 2021. Through this RG, the mandatory calendar for several groups of taxpayers to adhere to the SIFEN was established, foreseeing ten groups with nine different due dates, with a difference of one quarter between the dates foreseen for one group and another, except for groups 1 to 3, according to the following calendar.

| Groups | Date from which they are obliged |

| 1 – “Pilot plan” | July 01, 2022 |

| 2 – “Voluntary adherence” | July 01, 2022 |

| 3 – “Compulsory phase” | January 02, 2023 |

| 4 – “Compulsory phase” | April 03, 2023 |

| 5 – “Compulsory phase” | July 03, 2023 |

| 6 – “Compulsory phase” | October 02, 2023 |

| 7 – “Compulsory phase” | January 02, 2024 |

| 8 – “Compulsory phase” | April 01, 2024 |

| 9 – “Compulsory phase” | July 01, 2024 |

| 10 – “Compulsory phase” | October 01, 2024 |

Obligated taxpayers from groups 3 to 10 may start issuing electronically before the established date in case they wish to do so gradually. However, once the mandatory date arrives - January 2, 2023, for group 3 - they must exclusively issue all their documents electronically since the authorization and stamping of their pre-printed or self-printed documents, granted by the SET, will cease to be valid, except for the one related to virtual withholding receipts.

Taxpayers should take into account that they will bear the cost of the development and implementation of an electronic invoicing system, which often involves a considerable implementation time, as acknowledged by the SET in article 4 of the RG when it grants a period of up to 12 months of adaptation to those who wish to become voluntary electronic billers.

Therefore, it is extremely important to be aware of whether you or your company is covered by the mandatory SIFEN, because, if you are and you do not take the appropriate measures in time, you may no longer be able to operate normally. If you want to know if you or your organization are affected by this RG, you can consult the complete list of taxpayers in the complete list of taxpayers in the following search engine. For further details or better advice, don't hesitate to get in touch with our tax professionals.