Executive Summary

| Regulation | Content | Date |

| Binding Consultation | The Undersecretariat of State for Taxation (“SET” per its Spanish acronyms) ruled on the application of Value Added Tax (“VAT”) to the acquisition of software and payment of fees for teachers from abroad by an educational entity recognized by the Ministry of Education and Science (“MEC”). | First semester 2023 |

| Binding Consultation | The SET ruled on the invoicing and tax treatment of VAT applicable to an assignment of receivables and payment of interest. | First semester 2023 |

| Binding Consultation | SET indicated the tax treatment of the investment in a mutual fund and the interest generated in the Personal Income Tax (“IRP”) for a natural persona with fiscal residence in Paraguay. | First semester 2023 |

| Non-Binding Consultation | SET established its position on the possibility of using bank transfer slips to support the cancellation of invoices on credit. | First semester 2023 |

More information:

► Response to a Binding Consultation on the application of VAT on the acquisition of software and payment of fees for teachers from abroad by an educational entity recognized by the MEC

The SET responded to a binding consultation made by a taxpayer; an educational institution recognized by the MEC. The taxpayer explained when submitting its consultation that, since the Covid-19 pandemic, it has been developing teaching methods involving virtual platforms. To this effect, it makes payments for the acquisition of software to use a digital platform and, in addition, pays fees to teachers located abroad who developed their educational activities both in face-to-face and virtual format.

The taxpayer argued to the SET that these operations are exempt from VAT, considering they relate to its educational activities. To this effect, it cited article 100, paragraph 6 of Law No. 6,380/2019 (the "Tax Law"), which exempts from VAT the importation and sale of certain goods related to education services, when they are carried out in favor of educational entities.

In response to this consultation, the SET determined that two transactions are being carried out simultaneously by the taxpayer: (1) hiring of teachers from abroad for the development of educational activities in a virtual and face-to-face format, and (2) acquisition of licenses for the use of software from abroad to access virtual platforms.

Regarding the first operation, SET replied to the taxpayer that hiring teachers to render teaching services is exempt from VAT under article 100, numeral 3, paragraph “g” of the Tax Law.

Regarding the second transaction, the SET replied that this transaction is included within the "digital services" concept of the Tax Law, specifically within Article 12, paragraph "b" of General Resolution No. 76/2020. In other words, in this case, the SET understood that the category of digital service prevails over that of education, and, therefore, the exemptions for education services do not apply to the acquisition of software licenses to access virtual platforms, even when these platforms are for education purposes.

Consequently, the SET replied that the entities that intermediate the payment of software licenses to access virtual platforms are obliged to act as VAT collection agents, considering that the taxpayer explained that he makes the payments with bank transfers.

The SET concludes its analysis by explaining that the VAT exemption for importing goods, equipment, and supplies by educational entities contained in article 100, numeral 6, of the Tax Law, invoked by the taxpayer, does not apply to the transactions in question. SET bases this position on the fact that such exemption only applies to the operations (import and sale) of physical goods included in such provision and therefore does not extend to the operations described by the taxpayer, which, since they are related to the use and transfer of software by electronic means, correspond to services.

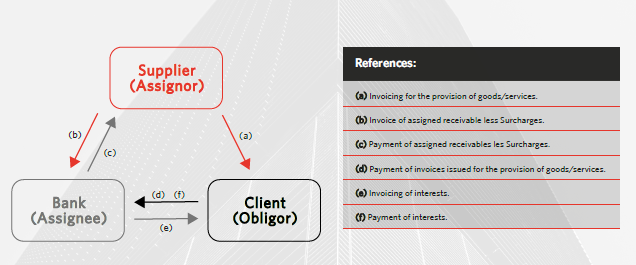

► Response to a binding consultation on the tax treatment of an assignment of receivables and interest payment transaction

A taxpayer asked the SET whether the interest and expenses generated in a credit assignment transaction are exempt from VAT. The taxpayer (“Supplier”) explained that it had entered into a service provision contract with another company (“Client”) and that it issued a credit invoice that was pending payment, so it assigned and transferred its collection rights arising from the provision contract to a bank (“Bank”) to advance the funds of the credit invoice.

This financing by the Bank generated expenses and costs, interest and administrative expenses, plus VAT (“Surcharges”), which the Bank charged to the Supplier by deducting them from the funds advanced to the Supplier in connection with the assignment of the credit, thus obtaining the Bank's result from the difference between the amount paid to the Supplier and the amount collected from the Client. The Supplier consulted SET on how to document the Surcharges of the credit assignment affecting operations (b) and (c) of the above image.

However, SET understood that the query did not refer to the Surcharges but to who is responsible for issuing the invoices when collecting the interest accrued after the assigned credit, which would be operations (e) and (f) of the above image. Due to this, SET addressed the consultation by indicating that two operations are being developed juxtaposed: (1) the assignment of the credit -(b) and (c)-, and (2) the collection of interest by the Bank or new creditor -(e) and (f)-.

Regarding the first transaction, the SET confirmed that the assignment of credits is exempt from VAT (article 100, numeral 1, paragraph "b" of the Tax Law). Regarding the second transaction, the SET indicated that the Bank or new creditor must issue the invoices for the collection of interest accrued after the assignment (article 81, numeral 2, paragraph “a” of the Tax Law). However, the SET should have addressed the original consultation on the documentation and taxability of the Surcharges for the assignment.

► Response to binding consultation on the tax treatment of an investment in a mutual fund and the interest generated by such investment

A taxpayer asked SET whether his investment in a mutual fund is deductible for determining his Personal Income Tax (“IRP”) liability. Additionally, he asked whether the interest generated by the mutual fund is exempt from tax, considering that the mutual fund invests the capital it receives in a portfolio of stocks and bonds.

Concerning the first question, regarding the possibility of deducting the investment in mutual funds for the determination of the taxpayer's income tax, the SET answered that, according to the provisions of the Tax Law, the income tax is divided into two categories, in practice, are determined and settled separately: (a) income tax on income derived from the rendering of personal services, and (b) income tax on income and capital gains ("IRP-RGC"). In this regard, SET explained to the taxpayer that the investment in mutual funds is not considered a deductible expense for any of the IRP categories.

About the second consultation, regarding the exoneration applicable to the interest received from the mutual fund, the SET answered that, effectively, the interest generated by the investment in the mutual fund corresponds to the IRP-RGC category, whose rules exempt it from this tax (article 56, numeral 11, of the Tax Law).

As an additional comment to what was resolved in the referred binding consultation, it is essential to point out that when a person invests in a mutual fund, the profit in the operation is obtained through the redemption of the quota part, with the order sent to the company that acts as administrator of the mutual fund ("AFPISA"). It is only at this moment when the AFPISA transfers to the investor the greater value generated in its quota parts as a result of the collection of interest and dividends obtained by the mutual fund that the referred exemption of the IRP-RGC would be activated if the investor is an individual with tax residence in Paraguay.

Before the moment indicated in the previous paragraph, the interests obtained by the mutual fund are not subject to Corporate Income Tax (“IRE”) since mutual funds are within the category of equity investment funds, which are considered as transparent legal structures (“EJT”), according to article 4 of the Tax Law. As an EJT, the income obtained by the mutual funds has a neutral tax effect in determining the IRE, so the interest earned by the mutual fund is not taxable for this tax either.

► Response to non-binding consultation on whether bank transfer slips can be used as payment vouchers to cancel invoices issued on credit

Through a non-binding consultation, a taxpayer asked SET whether any legal regulation establishes the use of the bank transfer slip as support for the cancellation of an invoice issued on credit. The taxpayer explains that he is making this consultation because he requested a money receipt for a payment he made to a supplier who had issued a credit invoice, which the supplier refused, arguing that the bank transfer slip is already the document that accredits the payment of the credit invoice issued by him, so he would not give a money receipt.

SET responded indirectly that there is no express legal tax regulation that regulates the use of bank transfer slips as support for the cancellation of an invoice issued on credit since neither this nor the money receipt are documents stamped by said institution.

However, despite this limitation, SET concluded that both the money receipt and the bank transfer voucher processed satisfactorily, due to their usual commercial use, can be considered as documents that serve as support for documenting, for tax purposes, the cancellation of invoices issued on credit by suppliers of goods and services.