Through Resolution No. 7, Minute No. 11, dated March 13, 2025 (the "Resolution"), the Central Bank of Paraguay established new caps on the fees applied for payment intermediation services made through credit or debit cards. This measure aims to align the Paraguayan market with international practices and promote financial inclusion.

According to the Resolution, the new limits will be applied gradually:

From July 1, 2025, the maximum fee will be 4% for credit cards and 3% for debit cards.

As of July 1, 2026, these caps will be reduced to 3% for credit cards and 2% for debit cards.

The decision is based on a technical analysis that identified current rates as being above regional standards. The reduction in commissions seeks to benefit businesses, especially small ones, by allowing them to access to electronic payment methods at lower costs, which could translate into more competitive prices for consumers.

Through Resolution No. 6, Minute No. 11, dated March 13, 2025, the Central Bank of Paraguay (“BCP”) introduced amendments to Article 20 of Resolution No. 43, Minutes No. 95, dated December 30, 2015, which regulates the collection of intermediation fees on debit and credit card transactions.

With this modification, issuing entities and/or operators must publish all intermediation fees applied to affiliated merchants on their websites, distinguishing between debit and credit card transactions. This information must be presented in a matrix that categorizes transaction amounts and average payment receipt values (tickets) and will be distinguished by type of card, whether debit or credit. Additionally, entities are required to continuously update the information on the fees charged, ensuring that merchants and the public have access to up-to-date and accurate data.

Furthermore, BCP will establish the maximum rate applicable to intermediation fees. It is clarified that this maximum rate encompasses the total sum of all intermediation fees charged during the payment process, regardless of the functions or means used by the entities involved. However, additional fees may be applied for services other than electronic payment intermediation, such as business management, fund flow administration, or data analysis, provided that acquiring these services is not mandatory to access intermediation services.

Issuing entities and/or operators must submit their fee policies applicable to affiliated merchants to the central bank within the first half of January each year. These policies must include at a minimum: (i) a technical justification for the applied fees or reasons for modification; (ii) a technical study supporting any variations; (iii) a description of the services provided; and (iv) a breakdown of fixed and variable costs, specifying the calculation methodology and the distribution of costs among fees, operators, and merchants within their respective networks.

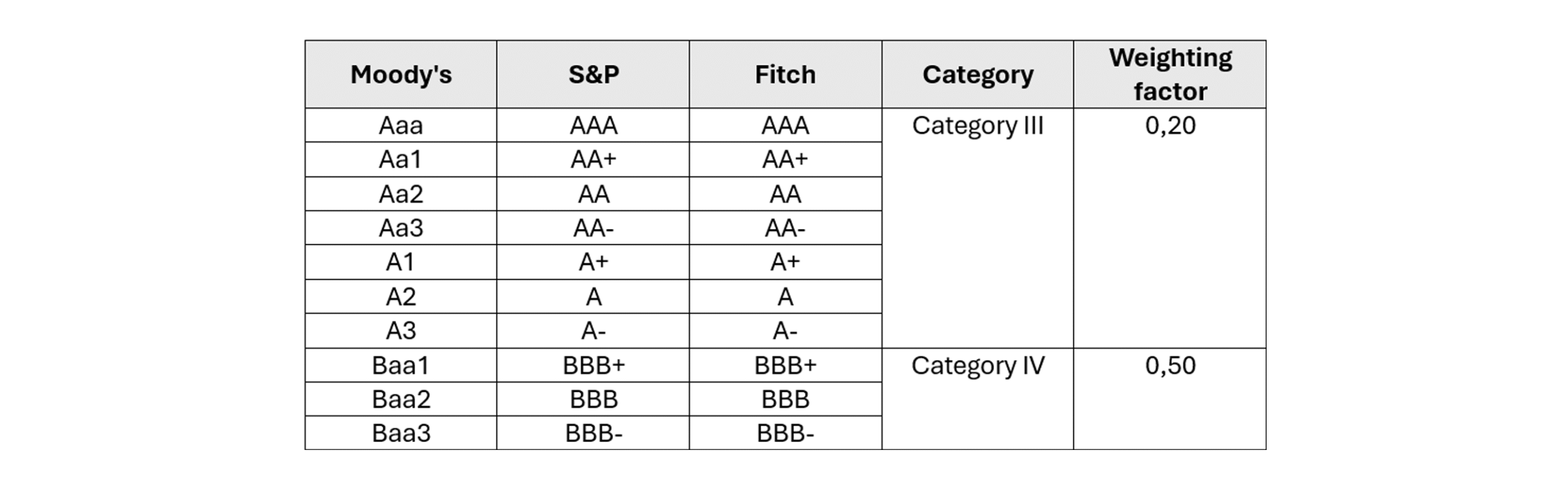

Through Resolution No. 3, Minute No. 16, dated April 15, 2025, the Board of Directors of the Central Bank of Paraguay ("BCP") authorized banking and financial institutions to purchase, hold and sell debt securities in foreign currency, issued by national governments and foreign financial institutions, provided such securities have an investment-grade credit rating granted by at least two of the following rating agencies: Fitch Ratings, Moody's or Standard & Poor's.

The regulation sets a global limit of up to 20% of each institution’s effective equity for holding these financial instruments. Furthermore, it establishes that, for the purpose of calculating capital adequacy indicators, investments in these instruments must be classified according to the risk rating of the issuing country, based on the weighting table defined in the same resolution:

Through Resolution No. 2, Minute No. 16, dated April 15, 2025, the Board of Directors of the Central Bank of Paraguay (BCP) amended various provisions of the General Securities Market Regulations (the "Regulation").

First, Chapter 2 of Title 26 "Depositors" of the Regulation, along with its Annexes A and B, was derogated. Article 9 of Chapter 12, Title 13 "Brokerage Houses" was also derogated.

Amendments were made to the definitions set forth in Article 1 of Title 26. The redefined terms include: (i) Depositors; (ii) Institution in charge of book-entry registration; (iii) Principal; (iv) Book-entry; and (v) Titles. The new definitions adopt more concise language and eliminate specific references to authorizations granted by the National Securities Commission.

Furthermore, Article 3 of Chapter 4, Title 3 “Brokerage Firms” was updated to define the securities admissible for over-the-counter transactions involving brokerage firms, both domestically and abroad. Among the most significant changes is the exclusion of Negotiable Custody Certificates (CCNs) from the list of securities admissible locally, while internationally, the previously established eligibility criteria were maintained.

On April 7, 2025, the Ministry of Public Works and Communications (Ministerio de Obras Públicas y Comunicaciones or “MOPC”) announced an ambitious road improvement project to connect the cities of Luque, Areguá, and San Bernardino with Route PY 02 (“Project”). With an estimated investment of USD 180 million, the Project will become the first rapid access and exit system aimed at optimizing mobility between the metropolitan area of Asunción, enhancing connectivity with the departments of Central and Cordillera.

Strategic Sections

The Project will be divided into three main sections:

Ypacaraí – Areguá – Luque Corridor: starting at Km 41 of Route PY 02, it passes through Ypacaraí, Patiño, and Areguá, reaching downtown Luque. It includes a new bypass in Areguá to optimize traffic flow.

Ypacaraí – San Bernardino – Luque (Tarumandy) Corridor: starting at Km 43, it connects San Bernardino with Luque. It includes lane duplication at the entrance to San Bernardino, urban improvements in the city, and lane expansions along the “Ecovía” section.

Elevated Expressway: a 4 km elevated stretch with 2 roadways and 4 lanes, connecting Luque’s urban area to the Conmebol area. This expressway will be compatible with the future commuter train and will preserve Luque’s urban dynamic.

Contractual Framework and Financing

The Project will be carried out under the addendum to the Public-Private Partnership (PPP) contract for the construction/expansion, operation, and maintenance of Route PY 02 (the “Works”), executed between the Paraguayan State and the Rutas del Este consortium (Sacyr and Ocho A), which was awarded the Works for a 30-year term. The addendum does not extend this term, so the Project must be executed within the remaining time of the original contract. Additionally, the addendum does not imply a direct award of the Project to the Rutas del Este consortium. The MOPC will launch a public tender process to award the execution of the Project. The selected company must secure 100% of the Project’s financing. However, the addendum grants the Rutas del Este consortium the right to match the best offer submitted by any bidder. Should it choose to exercise this right, Rutas del Este will be awarded the Project.

The tender is expected to be launched at the end of July, with the contract signing scheduled for August 2025. Construction is expected to begin by the end of 2025, with a projected execution period of three years.

The Works were carried out under Law No. 5102/13 on Public-Private Partnerships (PPP), which was recently repealed by Law No. 7452/25.

Repayment Structure

The investment repayment will be structured through three mechanisms:

Deferred Payments: semiannual payments over a 15-year period, beginning the month after 36 months from the issuance of the first notice to commence works.

Availability Payments: quarterly payments starting from the provisional commissioning of each section and continuing until the end of the contract.

Traffic-Linked Payments: variable payments tied to traffic volume in the covered sections, payable after the final provisional commissioning.

Impact

The project will benefit approximately 1.3 million people who travel daily through the metropolitan area of Asunción, reducing travel time by up to 30 minutes per trip in each section. This initiative marks a milestone in the modernization of Paraguay’s road infrastructure and opens new opportunities for private sector participation in PPP projects.

Esta publicación inaugura una serie de entregas sobre el marco regulatorio del sector energético en Paraguay. En esta primera parte, exploramos en detalle la legislación vigente, el rol de las instituciones clave y los elementos que marcan el rumbo del desarrollo energético nacional. Un material útil tanto para quienes operan en el sector como para quienes analizan oportunidades de inversión en energías renovables.

🔜 En la próxima entrega: un análisis práctico de los procedimientos de licenciamiento, los modelos contractuales vigentes y las principales barreras que enfrentan los desarrolladores de proyectos energéticos en Paraguay.

Para obtener más información respecto de alguno de los temas abordados en esta primera entregar, por favor póngase en contacto con nuestros expertos: Manuel Acevedo (macevedo@vouga.com.py); Rodolfo Vouga Z. (rgvouga@vouga.com.py); Yvo Salum (ysalum@vouga.com.py)

¿Cuál es la diferencia entre una marca evocativa y un signo genérico y por qué esto es importante? Resolución en el caso “Innovation Ventures LLC (“Innovation”) c/ Res. 206/2020 del 15 de abril y otra, dictadas por la Dirección Nacional de la Propiedad Intelectual (“Dinapi”)”.

Artículo y datos estadísticos OMPI – DINAPI

2025..

Datos estadísticos del año 2024 sobre registros de propiedad intelectual en Paraguay y a nivel internacional.

Noticias en el ámbito regulatorio

2025

DINAVISA incauta cosméticos sin datos del importador en el rotulado. Cigarrillos HNB (Heat Not Burn): Qué son y cómo los regula DINAVISA

More information

► Acuerdo y Sentencia nro. 156 de fecha 4 de noviembre del 2024, emitido por el Tribunal de Cuentas del Poder Judicial, Segunda Sala. Expediente: “Innovation Ventures LLC (“Innovation”) c/ Res. 206/2020 del 15 de abril y otra, dictadas por la Dirección Nacional de la Propiedad Intelectual (“Dinapi”)”.

Objeto y aspectos relevantes de la Resolución

¿Cuál es la diferencia entre una marca evocativa y un signo genérico y por qué esto es importante?

El pasado 4 de noviembre de 2024, el Tribunal de Cuentas, Segunda Sala (“TC”), emitió el Acuerdo y Sentencia nro. 156 (“AyS”), en el expediente Innovation Ventures LLC (“Innovation”) c/ Res. 206/2020 del 15 de abril y otra, dictadas por la Dirección Nacional de la Propiedad Intelectual (“Dinapi”). Mediante el AyS, el TC resolvió no hacer lugar a la demanda y confirmar las resoluciones recurridas.

La cuestión se originó cuando el 3 de diciembre de 2009, Innovation solicitó el registro de la marca “5-HOUR ENERGY”, tanto en clase 5 (para distinguir suplementos dietéticos) como en la clase 32 (para tragos energéticos, tales como bebidas energizantes). Ambas solicitudes fueron rechazadas por la Dinapi, al entender que el signo solicitado no era registrable por ser genérico. En efecto, el art. 2 de la Ley 1294/98, de Marcas (“Ley de Marcas”) establece que no podrán registrarse como marcas:

e) los [signos] que consistan enteramente en un signo que sea el nombre genérico o designación del producto o servicio de que se trate, o que pueda servir en el comercio para calificar o describir alguna característica del producto o servicio.

Luego de las apelaciones ante Dinapi que implicaron casi 11 años de proceso administrativo, el 16 de marzo de 2020 la Dinapi concedió el registro de “5-HOUR ENERGY”, en clase 5 pero no en la clase 32. Las resoluciones de rechazo de “5-HOUR ENERGY”, en clase 32 fueron apeladas por Innovation ante el TC. Es decir, la Dinapi tendió que “5-HOUR ENERGY” es genérica para bebidas energizantes, pero no lo es para suplementos dietéticos.

En este punto, cabe precisar que las marcas evocativas son registrables mientras que los signos genéricos, no lo son. En la práctica, no siempre resulta claro tener certeza acerca de si un signo es lo primero o lo segundo. Inclusive el criterio de la Dinapi también difiere, según las autoridades de turno .

En el caso en cuestión, el TC entendió que “una denominación genérica o descriptiva es aquella compuesta por vocablos o expresiones que son habitualmente usadas en nuestro lenguaje” para concluir que en este caso específico la marca “resulta a todas luces descriptiva de las características o funciones del producto para el cual se solicita el registro”. También sostuvo el Tribunal que la marca “evidentemente pretende describir la características y funciones del producto”, por lo que “mal podría decirse que la denominación marcaria pretendida es simplemente evocativa”.

A su vez, el TC sostuvo que “los signos evocativos dan una idea de cuál es el producto o servicio en cuestión o sobre sus componentes o características. A veces más que una idea, se trata de una certeza, y esto es lógico puesto que, de lo contrario, la marca sería engañosa”.

Entonces, este AyS resulta relevante para conocer mejor lo que el TC entiende que es un signo genérico o descriptivo a diferencia de una marca evocativa. Como vemos, también es determinante tener en cuenta la cobertura del signo, vis-à-vis la denominación del signo para poder juzgar su genericidad. De la diferenciación adecuada entre una categoría y otra, depende que el signo sea registrado o no, con la consecuente pérdida o no de tiempo y recursos. Por ahora, no hay constancia que el AyS se haya apelado.

► Información sobre registros de propiedad intelectual en Paraguay y a nivel internacional. Comentarios sobre estadísticas oficiales disponibles en los sitios web oficiales de la Dirección Nacional de Propiedad Intelectual (DINAPI) y la Organización Mundial de la Propiedad Intelectual (OMPI).

Estadísticas 2.024: Aumento en registros internacionales de propiedad intelectual según la Organización Mundial de la Propiedad Intelectual (OMPI). Estadísticas de registros de propiedad intelectual en Paraguay.

La (OMPI) publicó recientemente las estadísticas de registros internacionales de propiedad intelectual correspondientes al año 2.024. A continuación, se destacan los aspectos más relevantes de los registros internacionales gestionados por la OMPI a través de sus principales sistemas: el Tratado de Cooperación en materia de Patentes (PCT), el Sistema de Madrid para el registro de marcas y el Sistema de La Haya para diseños industriales.

Sistema PCT: Realizando una comparación con el año 2.023, el número de solicitudes ascendió a 273.900, lo que se traduce en un aumento del 0,5% respecto del año anterior. Entre los principales países de origen se citan China, Estados Unidos, Japón, Corea y Alemania. Asimismo, entre los principales solicitantes se destacan Huawei Technologies, Samsung Electronics, LG Electronics, entre otros. En 2.024, la comunicación digital se posicionó como el campo tecnológico con mayor número de solicitudes PCT publicadas, alcanzando el 10,5% del total y desplazando a la tecnología informática (9,7%).

Sistema de Madrid: En 2.024, las solicitudes internacionales de marcas bajo el Sistema de Madrid crecieron un 1,2%, alcanzando 65.000 solicitudes. Estados Unidos lideró con 11.270 solicitudes, seguido de Alemania, China, Francia y Reino Unido. Principales solicitantes: L’Oréal, Novartis AG, Euro Games Technology, entre otros. Principales clases en las que fueron solicitadas: equipos y programas informáticos y otros aparatos eléctricos o electrónicos.

Sistema de la Haya: En 2.024, el Sistema de La Haya para la protección internacional de diseños industriales registró un récord de 27.161 diseños, marcando un crecimiento del 6,8% por cuarto año consecutivo. China lideró con 4.870 diseños, seguida de Alemania, Estados Unidos, Italia y Suiza. Principales solicitantes: Procter & Gamble, Samsung Electronics, Porsche AG entre otros. Rubros principales: equipos de grabación y comunicación, medios de transporte, envases y embalajes, mobiliario, artículos para el hogar.

Estos datos reflejan un crecimiento significativo en las solicitudes de marcas, diseños industriales y patentes a nivel global. Los datos muestran una tendencia al alza en los sectores de tecnología, diseño y marcas, con un notable crecimiento en áreas como la comunicación digital, equipos y programas informáticos. De esta forma, se evidencia una mayor conciencia sobre la importancia de la protección de la innovación en un mercado cada vez más competitivo.

Paraguay:

Realizando un paralelismo con Paraguay y teniendo en cuenta que en nuestro país no se aplican los sistemas PCT ni el de Madrid, la página web oficial de la Dirección Nacional de Propiedad Intelectual (DINAPI) registró los siguientes datos durante el año 2.024:

Solicitud y registro de patentes: en el 2.024 se presentaron 381 solicitudes de patentes, de las cuales, 13 corresponden a solicitantes nacionales y 368 a extranjeros. En cuanto a concesiones de patentes, totalizan 42 (1 nacional y 41 extranjeros).

En comparación con el año 2.023, las solicitudes de patentes aumentaron un 7,94%, mientras que las concesiones crecieron en un 10% aproximadamente.

Solicitud y registro de marcas: durante el año 2.024 se presentaron 27.330 solicitudes de registro. De estas, 16.635 corresponden a solicitantes nacionales y 10.695 a solicitantes extranjeros. La clase con mayor cantidad de solicitudes es la 35, con un total de 4.380, seguida por la clase 5, que registró 3.370 solicitudes. En cuanto a concesión de marcas, la DINAPI reporta un total de 24.382 registros concedidos, de los cuales 12.066 corresponden a titulares nacionales y 12.316 a extranjeros. De nuevo, la clase 35 es la más solicitada.

En términos de crecimiento, las solicitudes de registro de marca aumentaron un 8,5% en comparación con el año 2.023, mientras que las concesiones de registros de marca crecieron un 33,8%.

Solicitud y registro de dibujos y modelos industriales: se registraron 164 solicitudes en total, 19 nacionales y 145 extranjeras. Concesiones: 153 en total, de las cuales 10 son nacionales y 143 extranjeras.

En comparación con el año 2.023, se visualiza un descenso del 15% en la cantidad de solicitudes, en cambio, en cuanto a concesiones se registró un aumento del 48% respecto del año anterior.

Los datos reflejan un crecimiento notable en solicitudes y concesiones de marcas, patentes y diseños industriales en Paraguay, especialmente en marcas, donde se ve un incremento importante en las concesiones. Sin embargo, la alta concentración de solicitudes de patentes y marcas por parte de solicitantes extranjeros sugiere que, si bien el país está siendo visto como un mercado atractivo, la innovación local aún tiene margen de crecimiento. Además, el descenso en las solicitudes de dibujos y modelos industriales podría indicar una falta de interés en proteger estos activos, aunque el aumento en las concesiones muestra una mejora en la eficiencia del sistema.

Para mayores detalles, favor seguir los siguientes enlaces: OMPI and DINAPI

► Derecho Regulatorio | DINAVISA incauta cosméticos sin datos del importador en el rotulado

Actualización sobre Normativas y Control de Productos Cosméticos

La Dirección Nacional de Vigilancia Sanitaria (“DINAVISA”) participó en la apertura de un lote de cosméticos incautados por el Ministerio Público, los cuales fueron puestos en cuarentena debido a la falta de información del importador en el etiquetado. Recordamos que este es un requisito obligatorio conforme a la normativa vigente en Paraguay.

Nueva Regulación para Productos Cosméticos

El pasado 2 de diciembre de 2.024, el Poder Ejecutivo promulgó el Decreto Nro. 2.942/2024, que reglamenta:

El artículo 39 de la Ley Nro. 1.119/1997, De productos para la salud y otros.

El artículo 5 de la Ley Nro. 6.788/2021, Que establece la competencia, atribuciones y estructura orgánica de la Dirección Nacional de Vigilancia Sanitaria, recientemente modificada por la Ley Nro. 7.361/2024.

Este nuevo decreto deroga el Decreto Nro. 3.636/2020, que regulaba previamente la obtención y renovación del registro sanitario para productos de higiene personal, cosméticos y perfumes, estableciendo un marco normativo actualizado.

Aspectos Claves del Decreto Nro. 2.942/2024

Entre los puntos más relevantes de esta regulación se destaca la facultad de DINAVISA para establecer estándares de rotulado y envase, garantizando la trazabilidad y control de calidad de los productos autorizados para su comercialización. Estos estándares ya están en aplicación dentro del mercado.

Importancia del Cumplimiento Normativo

Recordamos a los fabricantes, importadores y distribuidores la importancia de cumplir con las normativas de etiquetado y registro sanitario, ya que DINAVISA está facultada para realizar inspecciones en establecimientos de producción, importación, almacenamiento y puntos de venta, pudiendo proceder al retiro de muestras para análisis.

El incumplimiento de estas regulaciones podrá derivar en sanciones administrativas y legales.

Es posible acceder a la noticia haciendo click .

► Derecho Regulatorio | Cigarrillos HNB (Heat Not Burn): Qué son y cómo los regula DINAVISA

Los cigarrillos HNB (Heat Not Burn o “calienta pero no quema”) son dispositivos que calientan el tabaco en lugar de quemarlo, reduciendo la producción de humo y cenizas.

En Paraguay, la Dirección Nacional de Vigilancia Sanitaria (DINAVISA) regula estos productos conforme a normativas específicas que garantizan su calidad, seguridad y comercialización. Por ello, si utiliza o considera probar un dispositivo de calentamiento de tabaco (HNB), es fundamental asegurarse de que cumpla con los requisitos establecidos por la autoridad sanitaria.

La Resolución Nro. 153 del 11 de agosto de 2.021 establece los requisitos para el registro de los Vapeadores ante la DINAVISA y, además, fija los requisitos para la habilitación de los establecimientos dedicados a la importación, exportación, elaboración, distribución y comercialización de los Vapeadores. Al respecto, la Ley Nro. 6.788/21 y la Resolución Nro. 328/22 designan a la DINAVISA como autoridad sanitaria nacional responsable del cumplimiento de las disposiciones previstas en la Resolución y, en caso de incumplimiento, estará facultada a sancionar a los infractores.

[1] Por ejemplo, se encuentra vigente el registro marcario de “LÍQUIDO VITAL ABUNDANCIA AGUA PURA Y SALUDABLE” y Etiqueta, clase 32 (para aguas minerales); “OUT PAIN”, clase 5 (entre los que se incluyen productos farmacéuticos y veterinarios); “BIG ENERGY SHOCK” y etiqueta, clase 32 (para bebidas no alcohólicas), etc.

In a dynamic business environment, having clear and precise information is essential for strategic decision-making. Our Practical Guide Companies Paraguay provides a detailed analysis of key corporate aspects, offering a solid reference framework for those operating or planning to establish a business in the country.

This guide has been designed to systematically cover the main elements of Paraguay’s corporate legal framework, including:

Company Formation and Management: Legal requirements, shareholders’ rights and obligations, capital structure, and regulatory oversight.

Business Aspects: Tax, labor, and intellectual property obligations.

Registration Procedures: Steps for registering companies, branches, and joint ventures.

Corporate Structures: Characteristics, advantages, and costs of entities such as Corporations (Sociedad Anónima – SA), Limited Liability Companies (Sociedad de Responsabilidad Limitada – SRL), and Simplified Joint Stock Companies (Empresas por Acciones Simplificadas – EAS).

Our goal is to provide a practical and up-to-date resource that facilitates understanding of the regulatory framework and supports business development in Paraguay.

For more information about the guide, please contact Manuel Acevedo at (macevedo@vouga.com.py)

Through Resolution SV. SG. No. 04/25, dated March 6, 2025, the Superintendency of Securities ("SIV") amended Article 3, Chapter 9, Title 19 of the General Regulations of the Securities Market, establishing new deadlines for the submission of quarterly financial statements by management companies and investment funds.

With this amendment, management companies and investment funds must submit to SIV the financial statements of the management company and each fund they manage within 45 days after the end of each quarter, covering the following periods: (i) from January 1 to March 31; (ii) from January 1 to June 30; and (iii) from January 1 to September 30.

Through Resolution SV. SG. No. 03/2025, issued on March 6, 2025, the Superintendency of Securities amended Article 1, Chapter 3, Title 4 of the General Regulations of the Securities Market (“Regulation”), establishing new deadlines and requirements for the submission of annual periodic documentation that issuing corporations, publicly traded corporations, and other issuing legal entities must submit.

In this regard, the documentation that must be submitted within 30 calendar days from the approval of the Assembly is: (i) Board of Directors' Report with the qualified electronic signature of the legal representative; and (ii) Trustee's Report with the trustee’s qualified electronic signature, both in PDF format.

The documentation that must be submitted within 90 calendar days from the end of the fiscal year is: (i) Basic financial statements in electronic spreadsheet format, signed with a qualified electronic signature by the legal representative, trustee, accountant, and external independent auditor; (ii) External independent auditor’s report on the basic financial statements, in PDF format with the auditor's qualified electronic signature; (iii) Specific disclosures applicable to the financial statements’ accounts and accompanying notes, in PDF format with the qualified electronic signature of the legal representative, trustee, accountant, and external independent auditor; (iv) Report on related parties, in PDF format with the qualified electronic signature of the legal representative; (v) Annex B of Title 31 of the Regulations (basic financial statement models), duly completed in electronic spreadsheet format with the legal representative's qualified electronic signature; (vi) Statement of the company’s debts, in electronic spreadsheet format with the legal representative's qualified electronic signature (this provision does not apply to financial system issuing entities and cooperatives).

Companies that control more than 50% of another company’s capital must submit within 90 calendar days from the end of the fiscal year: (i) Consolidated financial statements in electronic spreadsheet format, signed with a qualified electronic signature by the legal representative, trustee, accountant, and external independent auditor; (ii) External Auditor’s Report on the consolidated financial statements, in PDF format with the auditor's qualified electronic signature; and (iii) Specific disclosures applicable to the consolidated financial statements’ accounts and accompanying notes, in PDF format with the qualified electronic signature of the legal representative, trustee, accountant, and external independent auditor.

Issuing companies that meet at least one of the following conditions may request their inclusion in a differentiated regime, with a deadline of 120 calendar days from the end of the fiscal year to submit the documentation mentioned in the third paragraph:

Adoption of International Financial Reporting Standards (IFRS); or,

Having outstanding issuances abroad at the end of the fiscal year.

The request must be submitted with the documentation justifying inclusion in the differentiated regime.